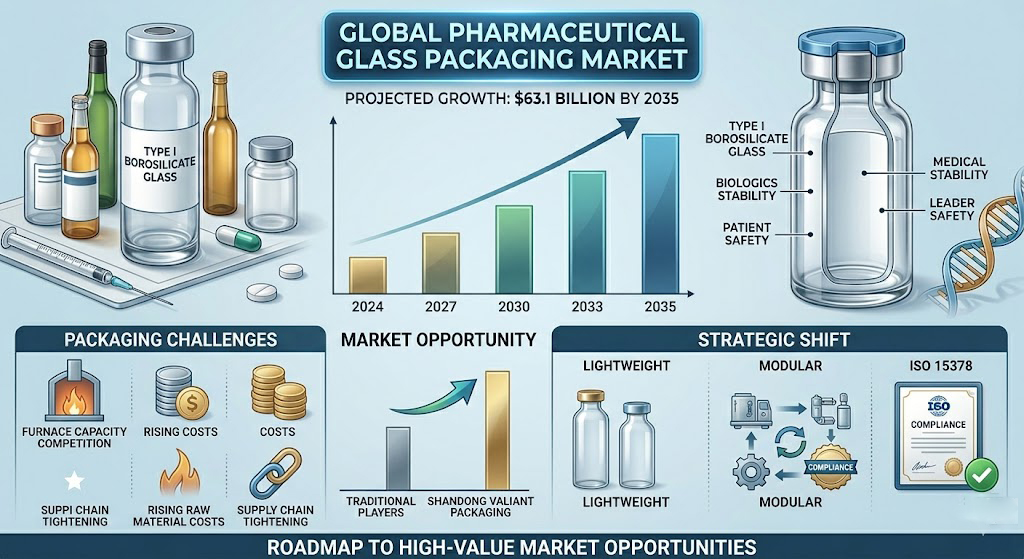

The rapid advancement of the biopharmaceutical industry, particularly the projected growth of the global pharmaceutical glass packaging market to $63.1 billion by 2035, is reshaping the strategic priorities of the glass manufacturing world. This surge is driven by a massive pipeline of biologics and biosimilars that require specialized Type I borosilicate glass to maintain product stability and patient safety. For the alcoholic beverage packaging industry, this development manifests as a significant “packaging crunch,” characterized by heightened competition for energy-intensive furnace capacity, rising raw material costs, and a tightening of global supply chains. The direct relevance to Shandong Valiant Packaging lies in the shared manufacturing ecosystem; as global leaders like SCHOTT and Gerresheimer pivot toward high-margin medical containers, a supply vacuum is created in the premium spirits and wine sectors that only technologically advanced, compliant manufacturers can fill. This report explores how the biopharmaceutical boom necessitates a shift toward “Lightweight Luxury,” modular manufacturing, and ISO 15378 compliance, offering a roadmap for B2B exporters to capture high-value opportunities in a supply-constrained environment.

Market Dynamics: The Biopharmaceutical Momentum and Global Glass Data Analysis

The global pharmaceutical glass packaging market is entering a phase of sustained, rapid expansion that is fundamentally altering the baseline for the container glass industry. In 2024, the market was valued at approximately $21.45 billion, with projections indicating it will expand at a compound annual growth rate (CAGR) of 9.8% to reach $39.82 billion by 2032. More recent industry assessments suggest even higher trajectories, with values reaching $42.02 billion as early as 2031. This growth is not merely volume-driven but is qualitatively defined by a shift toward high-value products. The Type I borosilicate glass segment, valued for its superior chemical resistance and thermal stability, led the market in 2025 with a 62.6% share, driven primarily by the surge in demand for injectable drugs and vaccines.

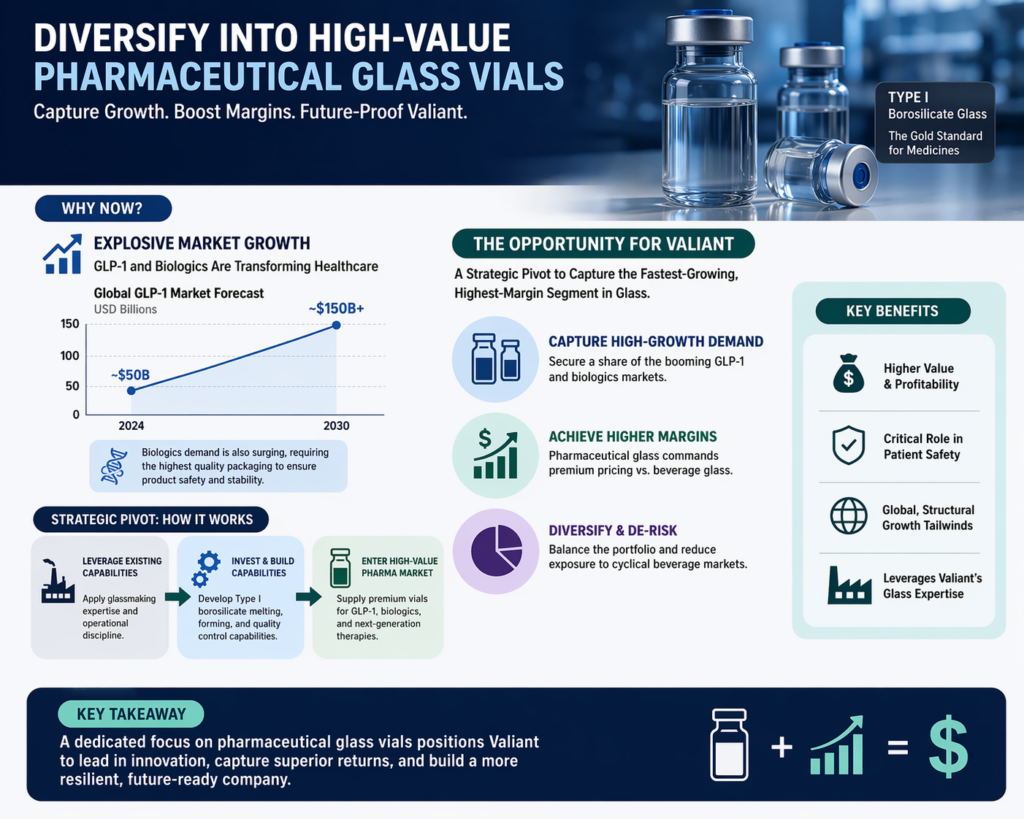

A critical catalyst in this expansion is the explosion of the GLP-1 (glucagon-like peptide-1) receptor agonist market. Global sales for these medications, which include blockbuster brands for diabetes and weight management, are forecast to rise from $76 billion in 2025 to $162 billion by 2031. Because these therapies are predominantly administered via injectables, they consume vast quantities of high-precision glass vials and prefilled syringes (PFS). This sustained pressure has created a two-tier supply system where demand frequently exceeds manufacturing capacity, particularly for sterile and ready-to-use (RTU) formats.

| Market Metric | 2024/2025 Value (USD) | 2031/2032 Forecast (USD) | 2035 Forecast (USD) | CAGR (%) |

| Global Pharma Glass Packaging | $21.45 Billion | $39.82 – $42.02 Billion | $63.1 Billion | 9.8% – 11.1% |

| Asia-Pacific Market Size | $6.8 Billion (est.) | $13.5 Billion (est.) | $21.2 Billion (est.) | 11.4% |

| North American Market Size | $7.8 Billion | $12.4 Billion (est.) | $18.6 Billion (est.) | 7.2% |

| Vials Segment Value | $8.4 Billion | $14.2 Billion (est.) | $19.1 Billion (est.) | 10.1% |

| Type I Borosilicate Share | 62.6% | 65.0% (est.) | 68.0% (est.) | 10.5% |

Regionally, the Asia-Pacific region is emerging as the fastest-growing hub, with a CAGR of 11.4%, supported by its role as a global manufacturing center for generic pharmaceuticals and vaccines. China and India are particularly dominant, consuming massive quantities of glass vials and ampoules for antibiotics and injectables. In contrast, the North American market, valued at $7.8 billion in 2025, is defined by a shift toward quality assurance and advanced coating technologies to prevent contamination in high-value biologics. European demand is increasingly dictated by sustainability mandates, such as the EU “Green Deal,” which requires all packaging to be reusable or recyclable by 2030, forcing glass makers to adopt carbon-efficient melting processes. These data points confirm that the glass packaging industry is no longer a commodity market but a technology-driven sector where capacity is increasingly reserved for the highest-value, most compliant applications.

Professional Interpretation: Impact on Beverage Packaging Materials, Costs, and Design

The biopharmaceutical surge exerts a direct and multifaceted impact on the beverage packaging industry, primarily through the mechanisms of capacity competition and material cross-pollination. As global glass manufacturers prioritize the production of Type I borosilicate glass for medical use, the available furnace capacity for traditional Type III soda-lime glass—the mainstay of the spirits, wine, and beer industries—is being squeezed. This has led to a “packaging crunch” in the food and beverage sector, where rising energy costs (now representing 18-25% of COGS) and supply disruptions are forcing brands to reconsider their packaging strategies.

One of the most significant implications is the accelerated adoption of “Lightweight Luxury” and “Right-weighting” in the spirits and wine sectors. Historically, heavy glass was the shorthand for premium quality; however, in 2026, sustainability and logistical costs have rewritten this equation. High-end brands are now pivoting to optimized silhouettes that reduce the carbon footprint and shipping costs without diminishing the aesthetic appeal. For example, industry initiatives like the Sustainable Wine Roundtable aim to reduce 750ml bottle weights to below 420g by the end of 2026. This trend mirrors the precision engineering found in the pharmaceutical sector, where material efficiency is critical for both performance and cost control.

Furthermore, the technological advancements required for pharmaceutical glass—such as specialized coatings to prevent leaching and AI-driven quality inspection—are trickling down into the premium beverage market. Digitalization and “Smart Packaging” are becoming central to the brand experience. Integration of NFC tags and QR codes, originally developed for pharmaceutical traceability and anti-counterfeiting, is now being used by brands like Johnnie Walker to verify authenticity and engage consumers through digital storytelling. As energy-intensive glass melting becomes more expensive in Europe and North America, manufacturers are also investing in modular manufacturing lines, such as the MAGMA system, which allow for faster capacity deployment and lower CAPEX compared to legacy furnaces. These innovations are essential for maintaining competitiveness in a market where the cost of energy and raw materials like soda ash and high-purity silica sand remain volatile.

Strategic Recommendations for Valiant Packaging: Seizing the Biopharmaceutical Opportunity

For Shandong Valiant Packaging, the advancement of the biopharmaceutical industry is a strategic signal to evolve from a high-volume glass exporter into a high-precision packaging partner. The proximity to the Shandong pharmaceutical manufacturing hub provides a unique advantage in terms of supply chain integration and technological spillover. To capitalize on these trends, Valiant should prioritize the following strategic initiatives:

Attain ISO 15378 Certification and GMP Compliance: As the lines between functional beverages, nutraceuticals, and pharmaceuticals blur, holding the ISO 15378 certification—which combines ISO 9001 with Good Manufacturing Practices (GMP)—will be a critical differentiator. This certification demonstrates a commitment to contamination control, traceability, and risk management that is highly attractive to premium spirits and wellness brands in the Americas and Europe.

Invest in Modular and Hybrid Melting Technologies: To hedge against rising energy costs and meet the sustainability demands of global beverage groups, Valiant should explore modular production lines like MAGMA and hybrid electric-gas furnaces. These technologies allow for smaller, more efficient “niche” production runs, which are ideal for the craft spirits and limited-edition wine markets that are increasingly seeking “Lightweight Luxury” solutions.

Lead in “Lightweight Luxury” and Sustainable Design: Valiant should leverage advanced forming techniques to produce “right-weighted” bottles that maintain a premium hand-feel while reducing glass mass. Developing proprietary silhouettes that integrate tactile elements—such as deep embossing and matte finishes—will satisfy the “Quiet Luxury” trend of 2026, where brand value is communicated through texture and ethics rather than bulk.

Adopt Smart Packaging and Traceability Solutions: Incorporating NFC tags and QR codes into the packaging design for high-value export lines will address the growing demand for authentication and consumer engagement in the North American and Southeast Asian markets. This also provides a future-proof pathway for complying with evolving European regulations on packaging transparency and recycling.

Diversify into High-Value Pharmaceutical Glass Vials: Given the explosive growth of the GLP-1 and biologics markets, Valiant should consider a strategic pivot or dedicated division for Type I borosilicate glass production. This would allow the company to capture a share of the fastest-growing and highest-margin segment of the global glass industry, diversifying the portfolio away from the more cyclical beverage market.

Conclusion and Outlook

The biopharmaceutical boom is fundamentally redefining the global glass packaging industry, transforming it from a commodity-driven sector into a field defined by technical precision and sustainability. The “packaging crunch” of 2026 is not a temporary disruption but a symptom of a broader structural shift toward high-value, high-performance materials. For B2B export traders, the opportunity lies in the convergence of these two worlds: applying pharmaceutical-grade quality and digital traceability to the premium beverage market.

Looking ahead to 2030-2035, the winners in the glass packaging space will be those who successfully transition to carbon-neutral manufacturing and modular production systems. As biopharmaceutical demand continues to consume vast quantities of furnace capacity, the premium beverage industry will increasingly rely on suppliers who can provide “Lightweight Luxury” without compromising on safety or aesthetic impact. For Shandong Valiant Packaging, embracing this strategic convergence is the key to securing long-term growth and leadership in the global spirits and wine supply chain.