Abstract

Table of Contents

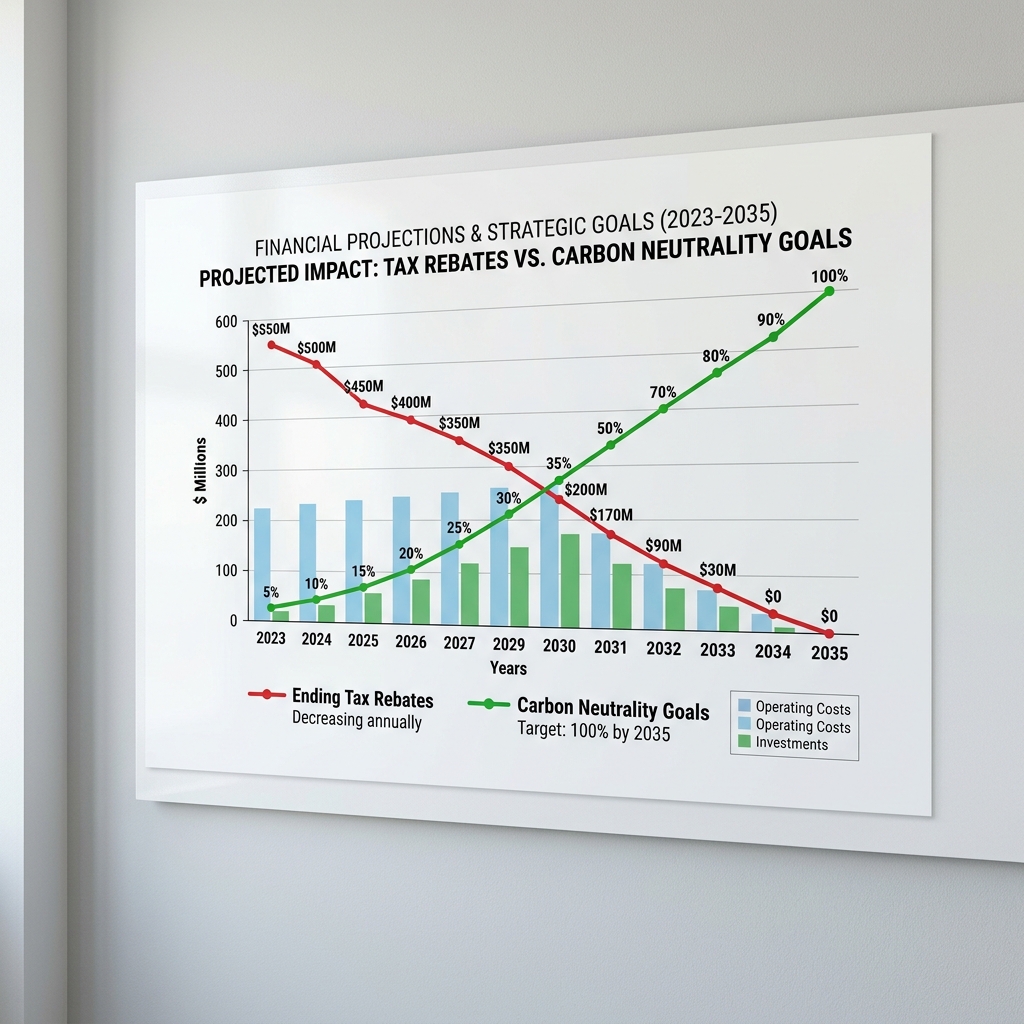

VAT Export Rebates in China have long served as the primary engine for industrial expansion, enabling domestic manufacturers to capture dominant positions in the architectural, industrial, and packaging glass markets through tax-advantaged pricing. However, the announcement in January 2026 that Beijing will systematically eliminate these VAT Export Rebatesmarks the definitive conclusion of the “tax rebate dividend” era. This transition represents a revolutionary recalibration of Chinese fiscal policy designed to address systemic overcapacity, resolve escalating trade tensions with Western economies, and align industrial output with aggressive carbon neutrality targets. As VAT Export Rebates are removed, the global supply chain is being forced into a rapid reconfiguration, characterized by the emergence of new manufacturing hubs in Vietnam, India, and Mexico, and a shift in supplier competitiveness from low-price volume toward high-tech, high-efficiency value creation.

The Historical and Fiscal Context of Chinese VAT Export Rebates

The architecture of the Chinese tax system has traditionally utilized non-neutral tactical levers for macroeconomic control. Unlike neutral frameworks in many Western economies where a zero-rate is applied to exports to ensure a full refund of domestic input taxes, the Chinese government has frequently adjusted the levels of its VAT Export Rebates to meet shifting national industrial policy goals. Between 2002 and 2012, approximately 87% of all products at the HS6 level underwent at least one upward or downward adjustment to their refund rates.

For the glass industry, these refunds historically helped offset significant manufacturing costs, logistics inefficiencies, and high energy expenditures. By allowing manufacturers to reclaim between 9% and 13% of their input tax, the system enabled Chinese products to be sold at prices that did not reflect their true production costs, facilitating the capture of over 40% of the global glass packaging market by 2025. However, the persistence of these incentives eventually became a point of contention, viewed by international trade partners as a discriminatory advantage.

Detailed Policy Breakdown: The 2026 Cancellation of VAT Export Rebates

The reform announced on January 9, 2026, by the Ministry of Finance and the State Taxation Administration represents one of the most consequential tax incentive adjustments in over a decade. The joint notice specifies the abolition or substantial scaling back of VAT Export Rebates for 249 categories of goods, with a heavy emphasis on industrial materials, solar components, and glass products. Effective April 1, 2026, the policy ends the practice of returning taxes to exporters, forcing a sudden increase in the cost of shipments from China.

For the glass sector, the policy applies broadly across HS Code Chapter 70, covering everything from basic architectural units to specialty industrial glass used in electronics. The impact is determined by the export declaration date: goods declared on or after April 1, 2026, are treated as domestic sales and subject to the standard 13% VAT without a refund.

Scope of 2026 VAT Export Rebates Cancellations in the Glass Industry

| Product Category | Specific Glass Items Included | Previous Rebate Rate | New Status (April 1, 2026) |

| Architectural Glass | Tempered, Laminated, Insulated, Low-E | 9% – 13% | 0% (Full Cancellation) |

| Industrial Glass | LCD Substrates, Conductive, Specialty | 9% | 0% (Full Cancellation) |

| Photovoltaic Glass | Coated Solar Glass, PV Module Covers | 9% | 0% (Full Cancellation) |

| Glass Containers | Soda-lime Bottles, Jars (>1L) | 9% | 0% (Full Cancellation) |

| Glassware | Drinking Glasses, Kitchenware | 9% | 0% (Full Cancellation) |

| Raw/Specialty | Optical Glass, Fiberglass, Ceramic Tiles | 13% | 0% (Full Cancellation) |

The financial consequence of this shift is a structural increase in export costs. The mathematical impact on pricing can be modeled by the following relationship:

Where r is the previous rebate rate. For a product that previously benefited from a 9% rebate, the factory must increase its price by approximately 9.9% to maintain the same net margin. For products that previously received a 13% rebate, the price must rise by nearly 15% to offset the tax loss.

Economic Rationale: Curbing Overcapacity by Removing VAT Export Rebates

The 2026 policy is also a critical component of China’s commitment to peaking carbon emissions by 2030 and reaching neutrality by 2060. The glass industry is one of the most energy-intensive sectors, and the removal of tax incentives acts as a “soft” carbon tax. By increasing the financial burden on energy-intensive production, the reform incentivizes factories to upgrade to advanced, high-efficiency equipment.

The 2024-2025 Action Plan for energy conservation specifically targets the glass sector, vowing to prevent the “blind initiation” of low-level projects. For the industry, the withdrawal of government support makes inefficient, coal-dependent production lines economically non-viable.

Market Disruption: The Short-Term “Landed Cost Shock”

The period leading up to the April 1 implementation is projected to be highly volatile. A “Pre-Change Rush” is expected between January and March 2026, as buyers attempt to lock in the final rebate-eligible prices. This surge is anticipated to mirror previous trends, with ocean and air freight rates potentially spiking by 20-30% due to capacity constraints.

Logistics and Freight Disruption Forecast (Q1 – Q2 2026)

| Impact Category | Anticipated Disruption Level | Key Details |

| Ocean Freight Rates | 20% – 30% Increase | Surge in volume at Shanghai and Ningbo ports |

| Air Freight Rates | 15% – 25% Increase | Driven by urgent shipments of high-value items |

| Customs Processing | 7 – 14 Days Delay | Caused by massive volume of Q1 declarations |

| Inland Trucking | 100% Premium (Doubling) | Capacity tightening in China’s industrial hubs |

| Container Availability | Significant Shortage | Mismatched lead times due to Q1 peak |

The “China Plus One” Strategic Reconfiguration

The disappearance of the “tax rebate dividend” is the final catalyst for multinational corporations to implement the “China Plus One” strategy. This involves diversifying production into alternative markets like Vietnam, India, and Mexico to mitigate dependency on China’s shifting fiscal landscape.

Vietnam has emerged as a primary beneficiary due to its extensive high-quality silica sand reserves in regions like Cam Ranh Bay and Quan Lan Island, where purity levels often exceed 98% $SiO_{2}$. Similarly, India is repositioning itself as a global export hub, with the glass market expected to grow at a CAGR of 7.7% through 2030. Saint-Gobain India, for instance, plans to increase its export share from 5% to 15% within five years, specifically targeting Southeast Asia and Australia.

Corporate Trajectories: Navigating a Post-Rebate Market

Industry leaders are adapting through global localization and high-value product focus.

- Fuyao Glass: Has responded by intensifying localization, investing nearly RMB 10 billion in “zero-carbon intelligent factories” in China and $700 million in North American automotive trim and float glass expansions.

- Xinyi Glass: Signed a $386 million agreement in 2026 to build Saudi Arabia’s first automotive glass factory, establishing a flagship production base to serve the Middle East and Europe.

- Vitro Architectural Glass: Is expanding its presence in the photovoltaic segment, including a $1.3 billion contract expansion to provide solar front sheets for North American module production.

Strategic Implications of Removing VAT Export Rebates for Global Procurement

The reconfiguration of the glass supply chain demands a shift in procurement strategy. Proactive buyers should implement the following mitigation plan:

- Supply Chain Audit: Assess exposure to the 249 HS codes affected by the loss of VAT Export Rebates.

- Inventory Buffering: Stockpile 20-30% extra inventory before April 2026 and extend lead times by 4-6 weeks.

- Supplier Vetting: Prioritize manufacturers with proven manufacturing efficiency and stable capacity rather than those who relied on tax refunds for pricing.

- Contractual Flexibility: Include clauses in new contracts that address national policy shifts in tax and tariff structures.

ValiantPackaging Strategy for the Post-Rebate Era

To navigate the abolition of VAT Export Rebates, ValiantPackaging (Shandong Valiant Packaging Co., Ltd.) should leverage its vertical integration to offset the ~10% effective cost increase through the following actions:

- Design for Efficiency: Use its in-house mold factory to develop lightweight glass containers that reduce raw material and energy costs.

- Premium Value-Add: Prioritize high-margin decoration services (metallic foil, frosting, silk-screen) that are less price-sensitive than basic glass.

- Operational Excellence: Integrate AI-driven quality control and logistics optimization to minimize waste and counteract freight surges.

- Green Compliance: Position itself as a strategic partner for European clients by providing documented sustainable manufacturing to qualify for green import incentives.

Conclusion: The New Rational Global Market

The removal of these tax incentives represents a structural shift in the glass export environment that is both inevitable and necessary. While it introduces immediate cost pressures, it marks the end of the “rat race” era and the beginning of a more rational, market-oriented global trade landscape. For the Chinese glass industry, this change is a driving force for high-quality development, forcing a transition from price-based competition to value-based innovation.