Abstract

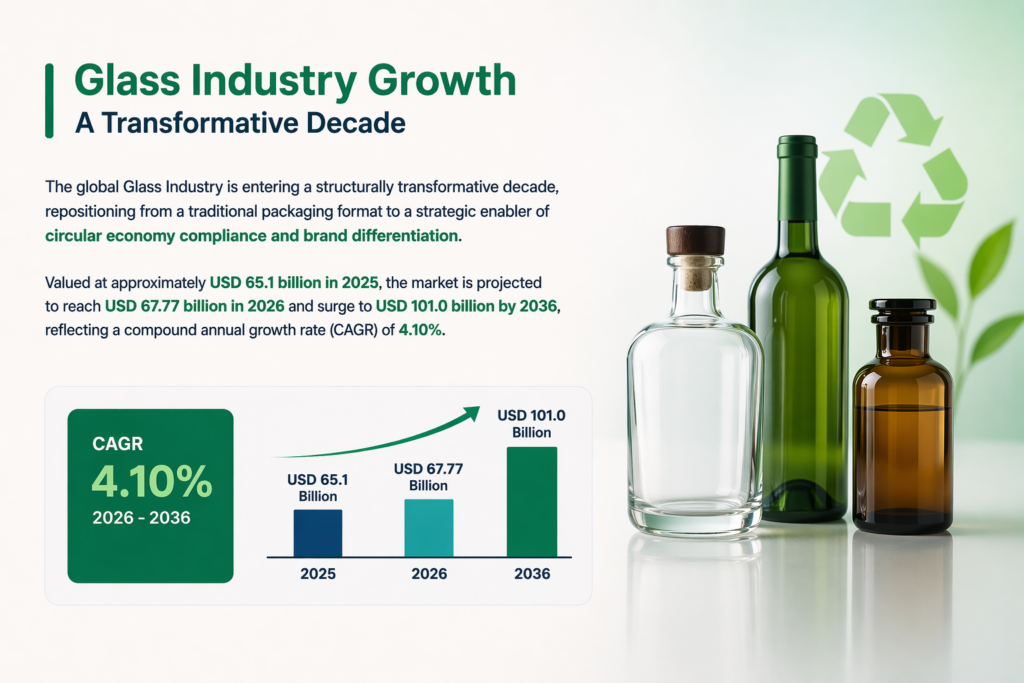

The global Glass Industry growth is entering a structurally transformative decade, repositioning from a traditional packaging format to a strategic enabler of circular economy compliance and brand differentiation. Currently valued at approximately USD 65.1 billion in 2025, the market is projected to reach USD 67.77 billion in 2026 and surge to USD 101.0 billion by 2036, reflecting a compound annual growth rate (CAGR) of 4.10%. This trajectory is of paramount importance to the packaging sector as it signals a move away from volume-driven production toward a value-driven ecosystem defined by sustainability, lightweighting, and digital quality control. For Shandong Valiant Packaging, this evolution offers a unique opportunity to leverage its vertically integrated infrastructure to meet the rising demand for high-end, sustainable solutions in the spirits, wine, and pharmaceutical sectors.

Global News and Data Analysis: The Statistical Trajectory of the Glass Sector

The Glass Industry growth is currently bifurcated between the regulatory-driven leadership of Europe and the volume-driven expansion of the Asia-Pacific region. Europe remains the global glass industry leader in circular economy practices, characterized by high cullet (recycled glass) utilization and strict sustainability mandates that drive continuous innovation. Simultaneously, the Asia-Pacific region—holding a 34.0% market share—remains the fastest-growing geographical segment, with India (5.6% CAGR) and China (5.2% CAGR) leading the charge due to rapid urbanization and middle-class consumption. In North America, the focus is shifting toward nearshoring and automation to strengthen regional supply chains. Major incumbents like Owens-Illinois, Ardagh Group, and Verallia are consolidating their positions by investing heavily in the electrification of furnaces and closed-loop recycling systems to mitigate the impact of energy price volatility.

Global Glass Packaging Market Size and Regional Projections (2024–2035)

| Metric | 2024 (Base Year) | 2030 (Projected) | 2035 (Forecast) | Regional CAGR (%) |

| Global Market Value (USD Billion) | 78.48 | 102.31 | 120.90 | 4.4 – 4.5% |

| Asia Pacific Revenue Share (%) | 36.0% | 38.5% | 41.2% | 4.9 – 5.9% |

| Europe Revenue Share (%) | 28.5% | 30.2% | 31.8% | 3.0 – 4.2% |

| North America Revenue Share (%) | 22.0% | 23.5% | 24.6% | 3.7 – 4.1% |

| Latin America Revenue Share (%) | 8.8% | 10.1% | 12.3% | 4.56% |

Europe remains the geographical epicenter of technological leadership, but the Asia-Pacific region holds the largest revenue share at 36.0% as of 2023. China alone represents 41.6% of the Asia-Pacific glass industry market, driven by rising disposable incomes and a systemic shift toward Westernized consumption patterns in the premium spirits sector. Simultaneously, the North American market is witnessing a profound shift toward “Lightweight Luxury,” with the wine glass bottle segment projected to grow from USD 8.4 billion in 2025 to USD 13.1 billion by 2034. The structural dominance of the “Big Three”—Owens-Illinois, Ardagh, and Verallia—is being challenged and refined by their internal pivots toward Net Zero targets. Verallia has recently committed to a Net Zero trajectory by 2040, the first in the industry to align with the 1.5°C pathway. Ardagh Group has reported a 16% reduction in Scope 1 and 2 emissions since 2020, while O-I Glass achieved a 30% reduction in GHG emissions against its 2017 baseline. These achievements are underpinned by a significant increase in renewable energy procurement, with O-I reaching 51% global renewable electricity volume in 2024.

Professional Interpretation of the Glass Industry: Material Evolution and Economic Pressures

The Glass industry is translating these news facts into a radical redesign of the “Luxury” container. In 2026, the definition of premiumization is shifting toward “Lightweight Luxury,” where sustainability and sensory engagement define value rather than excessive glass weight.

Sustainability as a Cost Hedge: Higher cullet utilization is no longer just an environmental goal; it is an economic necessity. Utilizing 10% more cullet reduces melting temperatures, leading to a 3% energy saving and a 5% reduction in carbon emissions.

Lightweighting Technology: Innovations such as the Narrow Neck Press and Blow (NNPB) process are now glass industry standards, enabling weight reductions of 15-30% without compromising structural integrity. Ardagh, for instance, recently launched its lightest wine bottle at just 300g.

Material Demand: Glass remains the “gold standard” for chemically inert packaging, particularly in the pharmaceutical sector where demand for vials and ampoules is surging.

Comparative Analysis of Manufacturing Technologies and Their Impact

| Technology | Weight Reduction Potential | Energy Savings | Environmental Impact | Key Adopters |

| Narrow Neck Press & Blow (NNPB) | 15% – 30% | 10% – 15% | Lower logistics CO2 | Vetropack, O-I, Valiant |

| Hybrid Electric Furnaces | N/A | 50% – 60% GHG | Replaces 80% natural gas | Ardagh (NextGen), Verallia |

| Biofuel/Oxy-fuel Trials | N/A | 15% – 25% | Carbon neutral potential | O-I (Holzminden), Ardagh |

| Smart QR/NFC Integration | N/A | N/A | Traceability/Engagement | Luxury Spirits Brands |

The adoption of the NNPB process is a critical differentiator in modern global glass industry. By optimizing glass distribution within the mold, manufacturers can produce thinner-walled containers that are more resilient than their heavier predecessors. This technological shift is essential for the “Value Tier” resurgence in high-inflation markets, where Manufacturing Cost Arbitrage between Europe and Asia is becoming permanent. In Southeast Asia, particularly Vietnam and Thailand, the glass market is benefiting from this arbitrage, with regional CAGRs exceeding 2.2% as beverage giants like Heineken and ThaiBev shift capacity to more cost-efficient hubs. Furthermore, the pharmaceutical sector in Indonesia is driving demand for specialized Type 3 and Type 1 borosilicate glass, projected to reach USD 11.7 billion by 2025, emphasizing the need for chemical inertness and long-term stability.

Strategic Recommendations for Valiant Packaging: Navigating 2026 and Beyond

Shandong Valiant Packaging is uniquely positioned to capitalize on these trends through its expansive, vertically integrated business model. As of 2022, the group has scaled to include six glassware manufacturing companies, two post-processing companies, and its own sea freight forwarding company. This structure allows for an agile response to the “Value Tier” resurgence in high-inflation Western markets.

- Leveraging Vertical Integration: Valiant should utilize its in-house mold manufacturing and post-processing capabilities (including screen printing, spray coating, and hot foil stamping) to offer rapid prototyping and high-end customization. This allows brand owners to achieve the “Tactile Dopamine” moment required in 2026 luxury design without the lead times associated with fragmented supply chains.

- Capitalizing on Pharma and Food Safety: With certifications such as ISO 15378:2017 (primary packaging for medicinal products) and FSSC 22000 (food safety), Valiant should aggressively target the high-growth Southeast Asian pharmaceutical and premium food jar segments.

- Logistical Certainty: In a market where 2026 freight rates are moderating but systemic reliability is the primary concern for shippers, Valiant’s internal freight forwarding capability is a decisive competitive moat. Providing “land-to-sea” integrated solutions mitigates the risk of port congestion and inventory gaps for global partners.

- Sustainability Branding: By formalizing its “Climate Resilience” goals—focusing on electrification and low-carbon fuels—Valiant can align with the European PPWR mandates, making it a preferred partner for global beverage giants.

Strategic Blueprint for Global Expansion

- Technological Integration of “Lightweight Luxury”: Valiant must prioritize the deployment of NNPB technology across its spirits and wine bottle lines. The “Quiet Luxury” trend in Australia and North America for 2026 rewards brands that combine ethical footprints with sensory engagement. Valiant should market its 3000+ existing molds not just as variety, but as a platform for “Right-weighted” bespoke designs that lower logistics costs while maintaining the tactile “dopamine” moment for consumers.

- Sustainability as a Competitive Moat: Following the examples of O-I and Ardagh, Valiant should formalize its “Climate Resilience” goals by increasing cullet (recycled glass) utilization. Utilizing 10% more cullet directly translates to a 5% reduction in carbon emissions and a 3% saving in furnace energy. Establishing a localized cullet sourcing strategy in export destinations like Southeast Asia could reduce the carbon intensity of the final product, helping clients meet ESG reporting requirements.

- Targeting Emerging Sector Pockets: The pharmaceutical boom in Indonesia (6.3% CAGR) and the premiumization of spirits in Mexico (Tequila production up to 351M liters) represent high-margin opportunities. Valiant should utilize its ISO 15378:2017 certification (primary packaging for medicinal products) to pivot aggressively into the Southeast Asian pharmaceutical vial and ampoule market, where demand for borosilicate glass is outpacing supply.

- Logistical Resilience and Service Consistency: While freight rates are collapsing in 2026, supply chain certainty is becoming the primary metric for traders. Valiant should utilize its internal sea freight forwarding company to offer guaranteed lead times and inventory buffering for key clients in the UK and USA, mitigating the risk of periodic port congestion or geopolitical disruptions.

Conclusion and Future Outlook

The global glass container market in 2026 is poised at the intersection of traditional craftsmanship and disruptive industrial technology. While the “Big Three” in Europe and the Americas are setting the pace for decarbonization through electrified furnaces and biofuel trials, the market’s center of gravity is shifting toward regions capable of balancing high-speed innovation with price discipline. The decline of excessive weight in packaging signals a new era where intelligence, aesthetics, and ethics define brand value. For Shandong Valiant Packaging, the strategic imperative is clear: by integrating advanced lightweighting technologies and positioning itself at the heart of the “Value Tier” resurgence, the company can transform global macroeconomic challenges into a definitive market-leading advantage. The future of glass industry is not just clear; it is light, smart, and infinitely circular.